Lewis Wickes Hine “Shorpy Higginbotham, 14, greaser on the tipple at Bessie Mine” 1910

Still, if you didn’t know better, you’d get the impression that America was built by the rich. Why otherwise would its wealth have been allowed to be shifted away from the middle class, and to the rich, to the extent that it has over the past 3 or 4 decades? The disastrous consequences for American society should have been plain for everyone to see. America’s heyday started off in the 50s with a 90% highest income tax bracket, which was lowered to 70% in 1960 through the Tax Reduction Act. Today it is 35%, and today is anything but a heyday.

When inequality becomes so extreme that it induces poverty at the bottom, it kills societies. Or, to put it differently, where inequality is concerned, America is becoming a third world country. But it’s not going to be a smooth sailing transition. So far, people have been surprisingly docile, spurred on be endless stories of desolate street corners around which recovery beckons, but when markets go south and once again more cuts are announced alongside higher bonuses for bankers, something will obviously have to give.

That doesn’t mean we will see the same growth rates again that we did in for instance the 1960s, we’re too far into resource depletion and environmental destruction for that. But we can still establish a much more prosperous society than the one we see on the horizon today.

More details here from a piece former banker and lawyer Charles R. Morris published at Reuters. Proof, meet pudding.

The Middle Class’s Missing $1.6 Trillion

The United States was the world’s first middle-class nation, which was a big factor in its rapid growth. Mid-19th-century British travelers marveled at American workers’ “ductility of mind and the readiness…for a new thing” and admired how hard and willingly they labored. Abraham Lincoln attributed it the knowledge that “humblest man [had] an equal chance to get rich with everyone else.”

Most Americans still think of themselves as middle class. But the marketing experts at the big consumer goods companies are giving their bosses the unsentimental advice that the middle class is an endangered species. Restaurants, appliance makers, grocery chains, hotels are learning that they either have to go completely up-scale, or focus on bargains for the struggling and budget-conscious. [..]

For the last 15 years, an international consortium of economists has been building data bases on the income shares of the richest people in the developed countries, based on pre-tax market income including capital gains and tax-exempt income, and excluding government transfers. The American data reveals the greatest inequality by far, followed by Great Britain.

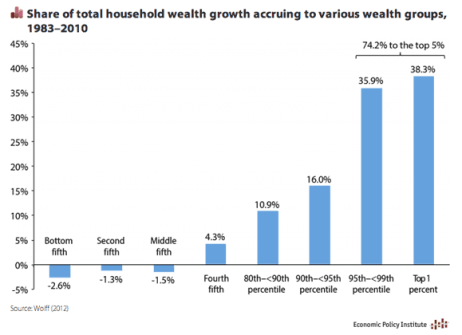

The stunning income distribution has a remarkable symmetry. In 2012, the top 10% captured half of all reported income. But the top 1% got almost half of that — 22.5% — while the top 10th of 1% (0.1%) captured half of that. All three are within a few decimal places of the previous highs — which occurred in 1928, just before the market crash that ushered in the Great Depression.

The stock market implosion of the 1930s followed by World War II’s strict price controls and high marginal taxes brought the top 1%’s income share down to about 9% by the end of the war. Executive and financial sector pay was quite restrained, even through the good times of the 1950s and 1960s, and the 1%’s income share did not start to rise until the late 1970s. It took off for the stratosphere then — amid the oceans of cash sloshing around Wall Street during the 1980s leveraged buyout boom.

[..] The difference between the 1%’s income share in 1975 (8.9%) and today’s 22.5% is 13.6%. That additional share of personal income is worth $1.6 trillion. Each year. To amass that incremental $1.6 trillion, the 1% took 68% of all personal income growth between 1993 and 2012. [..] … during the recovery of 2009-2012, they took a whopping 95% of the income growth …

The canonical retort to such musings is that all segments of society benefit from a well-fed and contented super-rich. Unfortunately, that is not proved true in recent experience. Since financial markets were liberalized in the 1980s, the finance sector’s income and debt has soared, income inequality has skyrocketed, and the world economy has flopped from crisis to crisis – the Savings and Loan fiasco, the petrodollar debacle, and the leveraged buyout circuses of the 1980s; the “hot-money” driven currency crises and hedge-fund collapses of the 1990s, and the hallucinatory mortgage games of the 2000s.

Adair Turner, the former head of the British financial regulatory authority, has outlined the “complexification” of finance that gave rise to the insane derivative structures and synthetic portfolios that unraveled so dramatically in 2008. Stephen Cecchetti and Enisse Kharroubi, two senior economists at the Bank for International Settlements, have documented the “inverse U-shaped curve” of finance’s contribution to the economy.

The history of all developed countries shows that as finance employment rises, economic growth and productivity increases. But only up to a point. After that, continued growth of the finance sector often triggers falling growth and declining productivity.

The two authors also worked out a model of why this happens. As the financial sector grows more sophisticated, it competes with technology and manufacturing industries for the smartest and most ingenious engineers and mathematicians. At the same time, however, broad-gaged finance needs highly “pledgeable” assets that can be readily leveraged, like residential and commercial mortgages. (High-technology investing has a very high risk of failure, and so is the preserve of specialist venture-capital firms.)

The best and the brightest, they found, instead of creating new technology breakthroughs, become the servants of the super-rich — because they pay the most. The engineers devote themselves to increasing low-productivity, easily understandable assets in order to transmute them into new, highly complex, instruments that look super-safe, but often aren’t. How to wreck an economy in three easy steps.

[..] … a key founder of the “University of Chicago School” of free-market economists, Henry Simon, opposed almost all government regulation, except for the financial sector. Simon understood that very smart people applying high leverage to other people’s money is an invitation to disaster, and so required tight regulation.

The most important step today might be breaking up the mega-banks that emerged from the crash. Then they would be easier to police — and easier to indict.

Second should be to start rolling back the income shares of the very richest people by targeted taxation and other strategies, including radical tax simplification to reduce the legal cubbyholes for sheltering income. The economist Brad DeLong wonders why the middle classes haven’t risen up and demanded fairer income distribution.

Reducing the top 1%’s income share to, say, 14 or 15%, still much higher than the pre-1980 norm, would free up about $1 trillion for middle-class tax relief; higher minimum wages; pension, healthcare, and educational subsidies, or job-creating infrastructure construction.

TLB recommends you visit http://www.theautomaticearth.com for more great articles and pertinent information.

See original article here: http://www.theautomaticearth.com/debt-rattle-feb-15-2014-kill-the-middle-class-kill-the-nation/

Leave a Reply